As investor and other like-minded individuals, we find it is not so much how much money you make, but how much money you save that will further assist in your investing and financial freedom goals. Today we share 7 of our favorite ways to save, to which we will break each one down. We will find how much you can save on a monthly/annual basis, as well as how much those extra funds can be worth further down the road. Life is great when you can dissect your expenditures and figure out new ways to save and open up more cash to invest!

1.) Grocery Store – Discount Grocer vs The BIG Box Grocer:

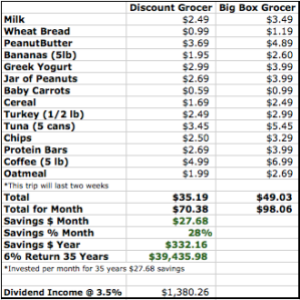

Lanny: We all love to eat nice food and try new things. However, for the most part, I try to eat relatively consistent when I am home and not traveling all over the place for work. I also try to eat extremely healthy and keep that lifestyle in tact, as I know how much better you feel when you are eating much cleaner/leaner and the energy it gives you. What’s funny is that people think that you need to shop at the big known name grocery store in order to think about eating healthy – that’s not the case here! Heck, I’m known for how Peanut Butter, Oats and Bananas are my recipe for Financial Success.

I have a local discount grocery store nearby that is far cheaper than the big box, yet I am still eating just as healthy as I would shopping there. The way this grocery store keeps their costs down is by: Less advertising, less employees and less overhead. They pass these savings on to the consumer! Here is the breakdown of the cost battle between the discount grocery store vs. the big box.

See the long term savings of $39,436 if you take the amount you save and invest on a monthly basis for 35 years at a 6% rate of return without any dividend increases:

2.) Buying a Conservative car vs. a Premium/Suped-Up model

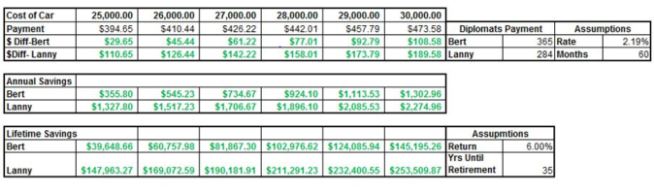

Bert: Every person can relate to this money saving tip. As our cars get older, rack up more miles, start to break-down, we are faced with the inevitable event of having to buy a new car. Both of us had to go through this as we purchased cars in 2013 (Bert purchased a new 2013 Toyota Camry and Lanny purchased a used 2010 Honda Accord). The first thing you see when you walk into a dealership are the brand new car models with all the bells and whistles. You test drive one of the nicer models and you suddenly can’t live without these features.

We are saying to FIGHT THAT URGE and purchase a more conservative car. For example, with my income level, I could easily have purchase a Camry with leather seats, GPS, etc. or a stripped down-Audi. Instead, I opted for the more affordable Camry SE with a purchase price of $22,000 (I now pay $365/month). The Camry had cloth seats, no sun-roof and no navigation (How on earth am I going to survive?). The decked out Camry or the stripped down Audi could have run me anywhere between $25,000 – $30,000 and would have resulted in a much higher monthly payment.

By saving on my monthly car payment, I am freeing up dollars to invest in my dividend portfolio and generate additional income via dividends. Here is the breakdown of the lifetime savings from purchasing conservative cars instead of premium models (also, see Lanny’s purchase which resulted in a $284/monthly payment, which he paid off his auto loan 18 months early!):

Note: We projected the savings over the 35 years because we will continue the practice of purchasing conservative cars the rest of our lives (if a car is even needed)! The lifetime return from a $25K car for Bert = $39,648 and $147,963 for Lanny, amazing!

3.) Your own Hair Cut!

Lanny: We are frugal. The average male will more than likely pay $20 a month for a haircut or $240/year. I cut my own hair every month and save the $20/month. Investing this $20/month every month for 35 years at a 6% conservative return rate = $28,494. That’s just the beginning. Invested into Dividend Stocks at a 3.5% dividend rate provides a $997 annual dividend income stream! Reach for those clippers.

See our Top 5 Foundation Dividend Stocks

4.) Brew your own coffee

Lanny: Working in the business world – there are quite a few co-workers who go for their typical big chain Starbucks Coffee.. every morning. Not just a traditional “black coffee” but typically a latte and a grande at that. The price of a grande latte, I assume, is essentially $4.00 every morning. These co-workers are spending $20/week on coffee, $20 for a satisfaction that may last one hour per day. I don’t mind the occasional Local coffee shop latte or special blend that day, but to me – it’s more of a treat. Too much of a good thing can “cloud” what a good thing tastes/feels like.

Additionally, the local coffee shops are cheaper than the SBUX coffee they are getting as well. However, I have been making my own coffee at home for some time now. If you are still in a bind for time – one can use the Keurig machine at home, which K Cups found on Amazon can even come in at $0.30-$0.35 per K-cup. If you drank one of these per day instead of grabbing the “white and green $4.00 cup”, you will only spend $1.78 during the week! That is a savings of $18.22 per week, $78.95 per month or $947.44 per year. If you invest this, on a monthly basis, at a very conservative 6% rate of return WITHOUT reinvestment for 35 years = $112,480! And if that dividend investments provides a 3.5% dividend yield, this provides you $3,937 in dividend income annually. I’ll skip the overpriced latte and reach for the cup. Oh and this Sumatra Fair Trade Certified Kona is my favorite roast.

Editor’s Note form Bert: I am a bit more of a coffee snub than Lanny. I buy whole bean coffee from a local coffee shop or grocery store and grind my own coffee. When I run out of coffee, I make a trip to Whole Foods and buy a pound of freshly roasted coffee. Instead of paying $10.99 per pound, I buy the coffee on sale that week for $8.99/lb. Each bag of coffee will produce between 45-50 cups of coffee, average to $.199/cup or $.179. Take that Lanny!

5.) Bonfire vs. Bar Night

Lanny: The last two weekends – a great group of friends (including Bert), have had bonfires instead of going out to the over-priced “scene”. If you are out and the average price of a drink on the weekends is $4.50, 4 drinks add up to $20 with tip. That’s if you are solo with no “rounds” being ordered, which happens usually once.

If you are with a girlfriend/significant other – lets double that if you happen to always treat. Boom, $40 now the night has tallied, in drinks alone. Sure, those nights are awesome, and fun. You get to try new places, see faces, meet new people – but doing that 1-2 nights per week adds up. Toss in a conservative $10 plate for 2, plus tip = $25, total for the night = $50.00

Alternative: Last night’s bonfire – I had two bottles of previously gifted wine that I’ve been wanting to drink. I picked up firewood, for $5. If you want to INCLUDE the the two bottles, the cost was $25. Now, two bottles of wine each served 5 drinks, so 10 drinks for the evening (when a glass of wine at a wine-bar/restaurant can cost, on the lower range, $6-$10/glass).

By doing this activity, we saved $25. We also ate at the bonfire, as that is what someone else contributed to the night! We ate, drank and hung out for 5 hours, without paying a valet or parking fee, for $25. If you ate, had 10 drinks and paid for parking = that is EASILY a $100+/night at a restaurant.

We had a view of Lake Erie, bonfire going, music and about 10 people total. If you could save $25 per week for 52 weeks, you’d have $1,300 in savings for a year. If you invest this every month for 35 years at a 6% return with no re-investment = $154,338 in value. This invested at a 3.5% dividend yield $5,400 in dividend income. Opt for the moment with friends instead of the “fad”. You will save money and build more divided income!

6.) Cut the Cord!

Lanny: This was described in my earlier post. In summary, you could save $50/month (pretty low approach as I know it’s typically higher) and save $600/year by ditching/not having cable. If you invest $50/month, every month for 35 years at a 6% rate of return, the value = $71,235 and at a rate of 3.5% = $2,493 in annual dividend income. Heck, take that money and invest into a telecommunications/cable provider in AT&T like we do!

7.) Packing a Lunch Vs. Buying

Bert: How many people have co-workers that buy their lunch everyday? I can think of at least 10 co-workers that buy their lunch from a local restaurant. I am all for supporting local businesses and I try to purchase goods from them every chance I get. However, racking up $8 lunch after $8 lunch can make a serious dent in your wallet and savings account.

Instead of buying your lunch everyday, pack your lunch! While your grocery bill may seem large, this is spread over MANY meals. This will be much cheaper than the $8 meal from a restaurant (most likely a healthier option as well!). Based on your individual shopping habits, here’s an analysis showing the savings if you were to choose to pack. It is time to bust out the Brown Bag!

Editor’s Note from Lanny: Bert, you spend at least $4.00 a day when you pack your lunch? What the heck are you packing yourself? All jokes aside, as you can see with my grocery list in bullet point number 1, I am a very frugal grocery shopper and I tend to pack relatively inexpensive lunches. I am a pretty consistent packer, so a typical lunch for me is as follows (Including the cost per item). Peanut-butter Sandwich: $0.20 for Bread + $0.11 for peanut-butter + $0.60 for 1 serving of Greek Yogurt + $0.39 for a 1lb banana + $0.20 for 1 serving of carrots. Total = $1.50 per day, savings of $6.50 per day, $32.50 per week, $140.83 per month or $1,690 per year!

Related: How Peanutbutter, Bananas and Oats are a Recipe for Financial Success

Using our current parameters of 35 years, investing every month at a conservative 6% rate without dividend reinvestment = $240,642 in value within that time frame! Further, at 3.5% yield, that provides $8,422 in dividend income. I’ll reach for the jar of Jiff before I reach into my pocket for plastic.

Summary

These are seven ways that the Diplomats have been able to increase savings and allocate more funds to dividend investing. If you apply the most frugal option in each scenario, YOU would have generated $773,469 (at an annual rate of return of 6% for 35 years)!! This would increase your annual dividend income and blaze you on the path to Financial Freedom. Even if some of these are not practical for you, push yourself to find new ways to save. As we discovered, even saving $1 per day for 20 days a month can turn into $28,500. Remember, every dollar counts in this game!

-The Dividend Diplomats