Last month I decided to take a plunge and accept the Dividend Diplomats’ Savings Challenge which pushes us and any brave reader to save 60% of their monthly income! This month I am going to try a slightly different method of displaying my savings rate. Last month, I listed the dollar amounts for each category used to calculate my final ratio. However, this month I am going to experiment with a new format (much like Lanny’s) and list each expense category as a percentage of total income for the period. With that being said, it is time to calculate my saving’s ratio for the month!

Savings Challenge Ratio

I am still trying to figure out the best way to project my monthly savings rate. Even though I now have a historical savings rate now, I still am not comfortable trying to project a monthly savings rate. Why? Because each month is filled with a different array of one-time events that can cause a sudden hit to your savings account. The volume of activities seems to fluctuate on a month to month and it depends on items such as the availability of my girlfriend and me. Also questions/potential items such as – what is going on in town for the weekend? Are we taking a vacation? Are there friends visiting that we want to entertain? All of the above, essentially. In September, our month was very busy and we were either hosting friends, visiting friends, or attending festivals each weekend, so naturally my expenses were greater. To contrast, we had a relatively quiet October. So until I have a few months under my belt, I do not want to set a benchmark savings rate for myself. I will wait until after December to do so and will allow me to use four months of savings data to develop a solid average. If you have any suggestions about this, please comment!

Last month, my final savings ratio was 48.56%. For the month of October, my savings rate was…Drumroll please…..62.69%! This was a 29.09% increase from the prior period. Holy cow, there we have it! I crossed the Dividend Diplomats savings challenge this month! One month down, hopefully many more to go. How did I achieve this feat? Let’s see!

Income

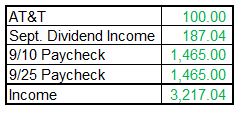

Last month I had three income sources: salary, dividends, and a $100 AT&T Rewards card. This month my income faced two downward forces and had a new income source. Let’s start with the downward pressures. First, the $100 AT&T gift card was a one-time reward so it will not be factored in this calculation going forward. Second, last month was the end of a quarter and you know what that means…it was the highest paying dividend month of the quarter. Since October is the first month, my monthly dividend income decreased from $187.05 to $117.40. While my income did decline this month, I am fortunate that the decline was not from my major income source and the overall bottom line was not damaged too badly.

As I mentioned earlier in the section, I have a new revenue source this month: Reimbursement for driving for work. When I travel, my company pays me the government rate of $.56/mile driven instead of reimbursing me for the cost of gas used in the trip. This policy helps reimburse the wear and tear that can be rather costly down the road. While September was a quiet month for me (I was not the driver on our business trips, so I did not benefit from this policy), I drove a lot for work in October. In total, I was reimbursed for four business trips; three of which were over two hours away. Let’s just say the Camry put on a lot of miles during this period.

{kind=link}

I broke down my expenses into the following categories and discussed my spending for each category below. As I discussed in the opening paragraph, I wanted to breakdown my expenses as a percent of income as opposed to the dollar amount that I used the last month. Please let me know if you do not like this new format! For comparative purposes, I re-formatted the September expenses into a percentage of total income to help ease this transition.

- Apartment: This includes my portion of rent, cable/internet, and utilities. There is no significant change this month outside of the decline in my utility bills. This change improved my savings rate by $15, so it was a small victory!

- Car: This includes my car payment and insurance. There were no changes in this category during the month.

- Entertainment: As I discussed last month, there was a lot going on in Cleveland. I attended concerts, beer festivals, had visitors, golf outings and even drove to Michigan to visit an old college friend. It was fun, but very expensive. A lot of these expenses were one-time events, so I knew my October entertainment expenses would not be as high. And boy was I right. This month my girlfriend and I spent a few more weekends relaxing and having “at-home” date nights. With the lack of events, concerts, and visitors, this was by far my most improved category. I won’t expect each month to be this low and I will try to attend every fun event possible, but the lack of activities this month was a major reason I was able to cross the 60% month.

- Gas: Ah gas. Does anyone else cringe every time they fill up their gas tank? I know I do. And this month, I was at the pump a lot. In the income section I mentioned that I was reimbursed for driving for four business trips. The income is great and I received a lot of it this month; however, as driving increases, so does my gas bill. While filling up a 15 gallon gas tank four time sounds like it was very expensive, it could have been a lot worse though. For the last few weeks gas has been hovering around $3.00/gallon; an incredibly low price when compared to prices earlier in the summer. So while I filled up more frequently than last month, it was at a cheaper rate. This probably shaved $3 off per fill up. I’ll take it! It is better than having to fill up more frequently when gas prices spike.

- Travel: Last month my girlfriend and I purchased a LivingSocial for a weekend getaway. This month, there were no such purchases.

- Cell Phone: I recently found out that my company has increased their reimbursement for cell phone bills. So now, my full plan is compensated instead of the 50% I had been receiving in the past. Another $0 category for the month. Until a change is made in this policy, I will no longer include this category in my analysis, since there will not be an expense.

- Food: The fact this category increased surprised me a little bit. I was on the road more for work and my meals were paid for, so why did my food bill increase? The most likely culprit is that we hosted our families for dinner several times this month and opted to cook meals together instead of eating out. Since our time wasn’t spent at events like last month, it seems the expenses have shifted from the entertainment expense category to the food category. At the end of the day, the cost of food for these kind of events are a heck of a lot cheaper than eating out, so I won’t complain too much.

- Other: The haircuts got me again! As I mentioned last month, I do not cut my own hair and instead have elected to pay a premium for this service. It is worth every penny!

Conclusion

Even after writing this article, I am still in shock. I saved over 60% of my income this month! It seemed like it would be such a difficult feat and I honestly thought it would take a lot longer to hit this month. But this month my bank account was hit with the perfect storm. I found new revenue streams through reimbursements for traveling and my expenses were cut down as the frequency of one-time events fell off of a cliff. However, it is not all fun and games for this Diplomat. While I hit 60% this month, what makes me nervous was that it took traveling a lot for work to accomplish this feat. If I removed the cash inflow received for my reimbursement on gas and the extra fuel costs associated with the travel, my savings rate would have fallen to 54%. This shows me that I am not quite ready to achieve a 60% savings rate on a monthly basis. There is still some work to be done, and you bet I will find new ways to increase my savings rate. But for now, I will celebrate crossing the challenge mark!

-Bert