Visa isn’t the only dividend paying stock you know? While V is a holding in many dividend growth investors’ portfolios, I wanted to take a look at an alternative option to see if the grass is possible greener elsewhere. It is time to roll up our sleeves, pull our AMEX card our of our wallet, and analyze American Express Company (AXP) .

Qualitative Assessment

Through review of the American Express’ (AXP) last earnings release, earnings call transcripts, and various articles, I put together the following summary of factors that are impacting the company

Positive Trends:

- In the last earnings release, management cited that Cardmember spending increased 9%. We are coming off of a unique period in this country which saw consumer spending declined significantly in the aftermath of the financial crisis. It is a positive trend to see consumer spending increase. This is great news for all players in the credit card industry and the overall United States economy. Let’s just hope that consumers don’t decrease their savings rate too much!

- Management is focused on increasing their business cardholders by offering stronger reward products. This could be a potential cash cow considering the way business spend money for traveling employees. I can attest to this first hand since I travel a lot for my job. I am able to earn a lot of credit card points by using a personal credit card for all expenses my employer will refund in full. I selected my business credit card based on the best available rewards points. If AXP can offer a competitive rewards program and capture the market, their major investment could pay huge dividends. Trust me; the amount businesses spend on travel can be insane. There is a lot of fee income to be unlocked by AXP if the rewards are strong enough.

- The company is continuing to invest in international growth to broaden its customer base. Expanding into areas with a growing middle class or a new consumer-spending driven market will help grow the customer base and challenge the industry’s major competitors. The company is investing a lot of money on international restructuring, so I would expect many changes and new developments on this subject in the coming periods.

- Warren Buffet owns 14% of the company. His love for dividends and investment in strong companies is well documented; I don’t think I need to elaborate on this point much more.

Negative Impact:

- This is not found in an earnings release but is from personal experience. American Express is not accepted by all merchants. In this plastic world we live in, customers are relying on their credit cards as their main payment source (I won’t dive into this, that’s a whole different argument). The fact that merchants do not always except an American Express card is a major competitive disadvantage for the company. Consumers are also driven by convenience and some may forgo earning both a Visa and American Express card, one of which isn’t accepted at every merchant, in favor of owning just a VISA that is accepted everywhere.

- The company is currently battling the Justice Department over the disclosure of merchant-fees charged by each credit card company. After reading about the lawsuit on in an article published on Motley Fool (“Massive Change Could be Coming at American Express Company” by Patrick Morris), the lawsuit could have a major negative impact on the company. If the ruling stands the merchant can disclose to the consumer the fees that each credit card vendor charges the business and “encourage” the consumer to use the lower cost card. This is meaningful considering AXP charges a higher fee to merchants for the various tools it offers its customers. AXP’s customer based could potentially take a major hit if merchants begin offering incentives for customers to use a lower-cost credit card. I don’t know all the details of the lawsuit; however the cliff notes that I read do not paint a great picture.

Quantitative Analysis

And now onto the fun part. Let’s run AXP through the Dividend Diplomat stock screener and see how well it performs against its peers. I don’t think this will be much of a surprise, but I am going to compare AXP against its two largest competitors, Visa (V) and MasterCard (MA). These three companies have by far the largest market cap in the credit card services industry and are fierce competitors.

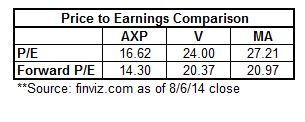

1. Price to Earnings Comparison. As indicated in our screener, we look for companies that have a P/E ratio below 15. Unfortunately, none of the companies fit the bill. AXP has the lowest P/E ratio of the group by a mile; however it is still above the mark used in our screener. It is worth noting that AXP has a lower P/E ratio than the S&P 500, which is approximately 19 on any given day. Who know, AXP may fall below 15 if the market continues to slide.

2. Payout Ratio. There is not too much to say about this metric other than all three companies have low payout ratios. This has allowed the companies to grow their dividend by such large margins (Read more below) oer the last several years. The payout ratio still remains relatively low with these increase due to the fact that each company also grows earnings at a comparable rate. Each company is very far under our threshold of 60% and has a lot of room to continue to grow their dividend going forward.

3. Dividend Increases. Again, all three companies have grown their dividend remarkably over their last five dividend increases. It is weird typing this sentence, but AXP has the lowest dividend increase by a large margin since they only have increased their dividend by 16.83% (on average) over the last five increases. Any dividend growth investor would love to have that kind of increase in their portfolio. However, the increase falls short when compared to the competition. This is where the Buffett factor comes into play. I am confident that AXP will continue to increase and maintain their current dividend yield as long as Buffett is a major shareholder. A growth rate of 16.83% is sustainable in the industry since earnings also grow at a similar rate. On the other hand, while the growth rates have been remarkable, I question whether V and MA can maintain the current dividend growth rate in the long run. At some point we will see their growth rate fall in line with AXP’s rate.

Summary

After performing my analysis, I have decided not to initiate a position and will instead just monitor the company going forward. After reviewing the companies market position and reading into the litigation the company is facing, it is easy to see why the company is trading at a discount compared to its peers (P/E is 7.38 less than V and 10.59 less than MA). Even with the discounted price, the company is still trading at a higher P/E ratio than the P/E used in our screener. In the past I have made exceptions and purchased stocks at a P/E greater than 15 and I only do so to purchase a company with a strong track record (such as PG). With the current market environment presenting opportunities in other dividend stalwarts such as Aflac (Lanny recently purchased some shares of the duck) and McDonalds, I think my extra capital can be better invested elsewhere. I also do not want to purchase any shares in the company until more information is available about the potential impact of the lawsuit with the government. It has the potential to severely impair the domestic customer base and will place a lot of reliance on the company’s growth abroad.

Does anyone hold shares in American Express? Am I being to cynical about the litigation’s impact on the company’s future earnings? Please let me know your thoughts, comments, and feedback.

Bert